Table of contents

TL;DR

A fund pitch deck is not a template you refine over time. It's a document that must be fundamentally rebuilt as your firm's stage of scrutiny changes. This guide walks through how narrative, slide structure, design language, and LP expectations shift from Fund I through Fund VI, and where most firms lose the raise in the gap between the two.

A fund pitch deck is not a template you refine over time. It's a document that must be fundamentally rebuilt as your firm's stage of scrutiny changes. This guide walks through how narrative, slide structure, design language, and LP expectations shift from Fund I through Fund VI, and where most firms lose the raise in the gap between the two.

Amélie Laurent

Product Manager, Sisyphus

LP sitting across the table at your Fund VI close. Your track record is strong. Three funds of consistent top-quartile returns. $600M deployed. You walk them through the deck. The narrative is polished. And then they pause at your performance slide and ask: "Where's the DPI breakdown by vintage?"

The number exists. Your team knows it.

But the deck doesn't show it, because the deck was built the way you built your Fund I deck, with a good story and a few highlight metrics. And in that moment, the LP isn't questioning your performance. They're questioning whether you understand what they need to see at this stage of the market.

That gap is where most raises slow down. Not because of what a firm has done, but because of how the deck presents it in relative to the level of scrutiny the firm is operating under.

Over a typical venture lifecycle, a firm moves from managing an $80M to $100M Fund I to deploying over $1B by Fund VI. That scale doesn't just change how capital is deployed. It changes how the firm is evaluated, who is in the room, and what those people need to walk away believing.

In early stage funds, the deck is doing one job: establishing credibility.

The emphasis is clear - who you are, what you see, and why you’ll win. The team, their experience, and a well-defined thesis carry most of the weight.

Design at this stage is focused on clarity. Its role is to make the narrative easy to follow.

By the time a fund reaches later stages (Fund V and beyond), LPs are no longer trying to understand who you are. They are deciding how much to allocate, and whether your performance holds up at scale.

This guide walks through how a fund pitch deck evolves across that arc: how the narrative changes, how slide structure expands, how design language shifts, and where the most common mistakes are made at each stage.

What LPs Are Actually Evaluating at Each Stage

The question an LP brings to a fund pitch deck changes significantly between Fund I and Fund VI. Understanding that shift is the foundation for building a deck that works.

At the early stage, LPs are working with limited data. The team hasn't built a track record yet.

The evaluation is centered on:

- a credible team with relevant operating or investing experience

- a clear, focused investment thesis

- access to the right opportunities

- a structured approach to building the portfolio

A 2024 Preqin study found that team quality and investment thesis were cited as the top 2 evaluation criteria by LPs reviewing emerging fund decks.

By Fund IV and beyond, that lens has shifted entirely. LPs are no longer asking whether the team can execute. They've already proven that. Now the question is whether the platform is built to deliver consistent outcomes at scale.

According to Cambridge Associates' 2025 benchmarking data, institutional LPs reviewing mature fund managers prioritize DPI, net IRR consistency across vintages, and evidence of portfolio construction discipline above all other factors.

7 Most Impactful Slides That Define How LPs Evaluate Your Fund

These are the slides where the evaluation happens. Each one is doing a different job depending on the stage, and each one has a distinct failure mode.

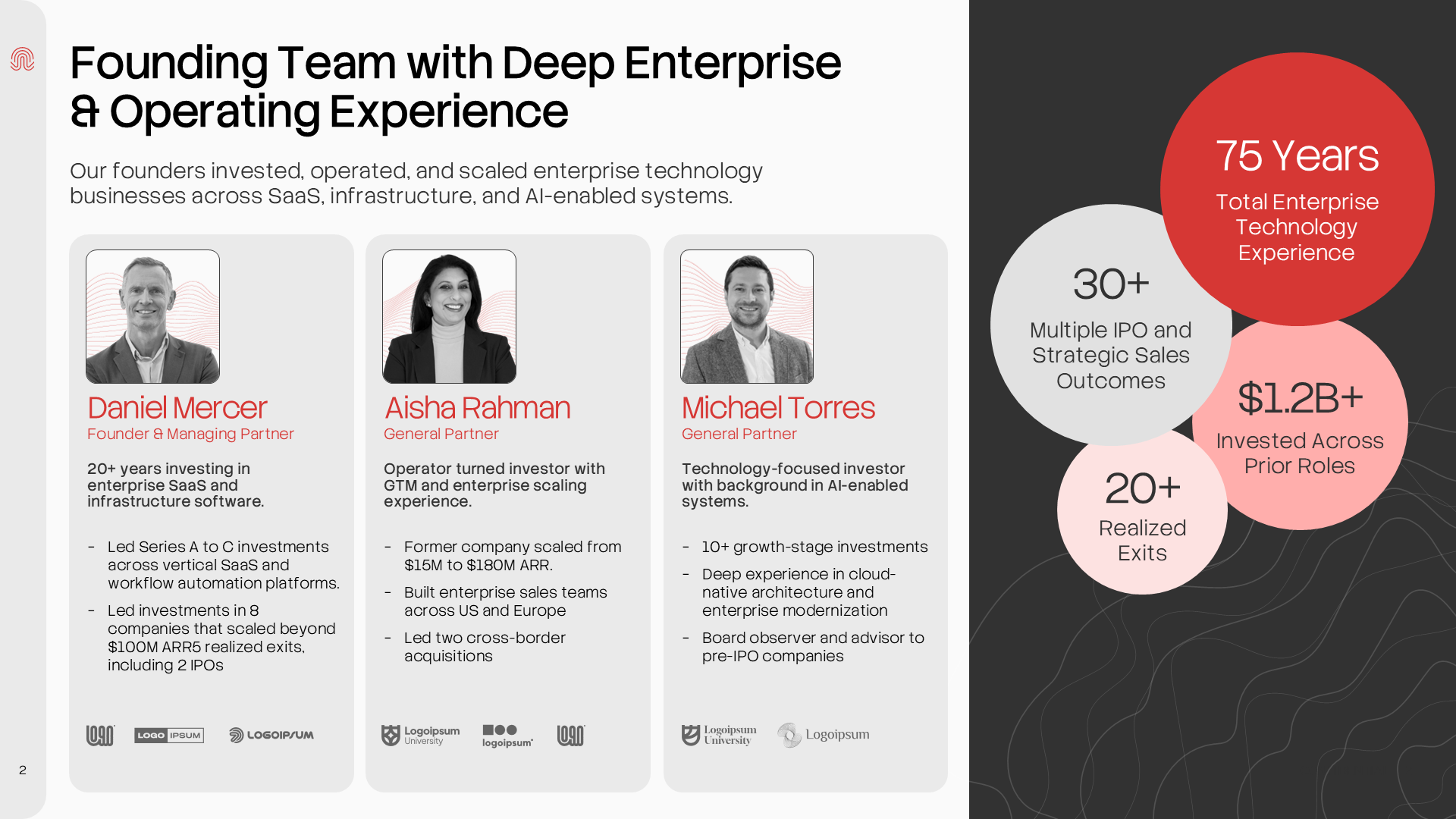

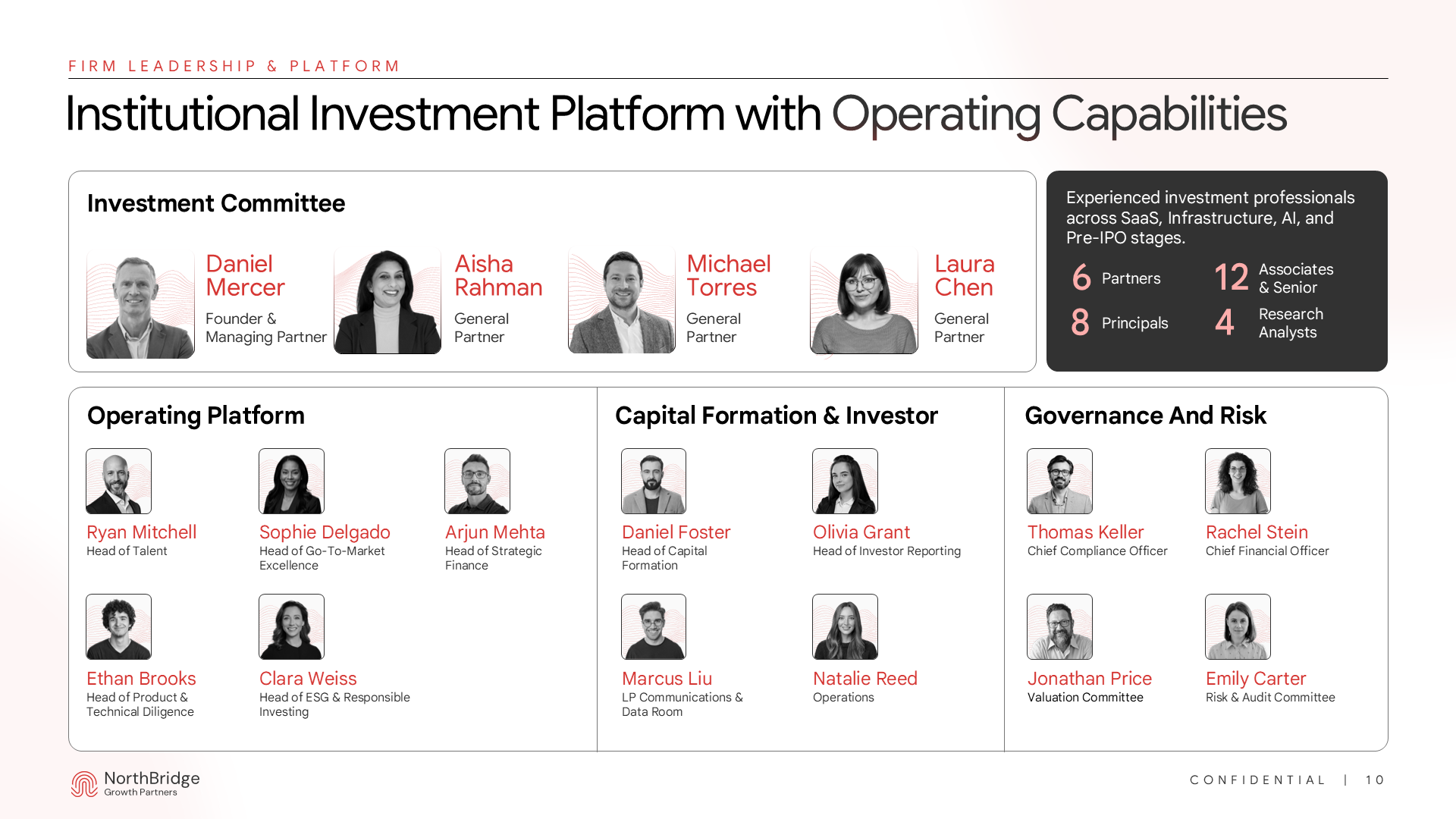

1. Team Slide

Early Stage

The story of who you are and why you're uniquely positioned to invest in this space. The team is the product.

Later Stage

Emphasis shifts to platform depth, investment team, operating partners, ESG function, LP relations.

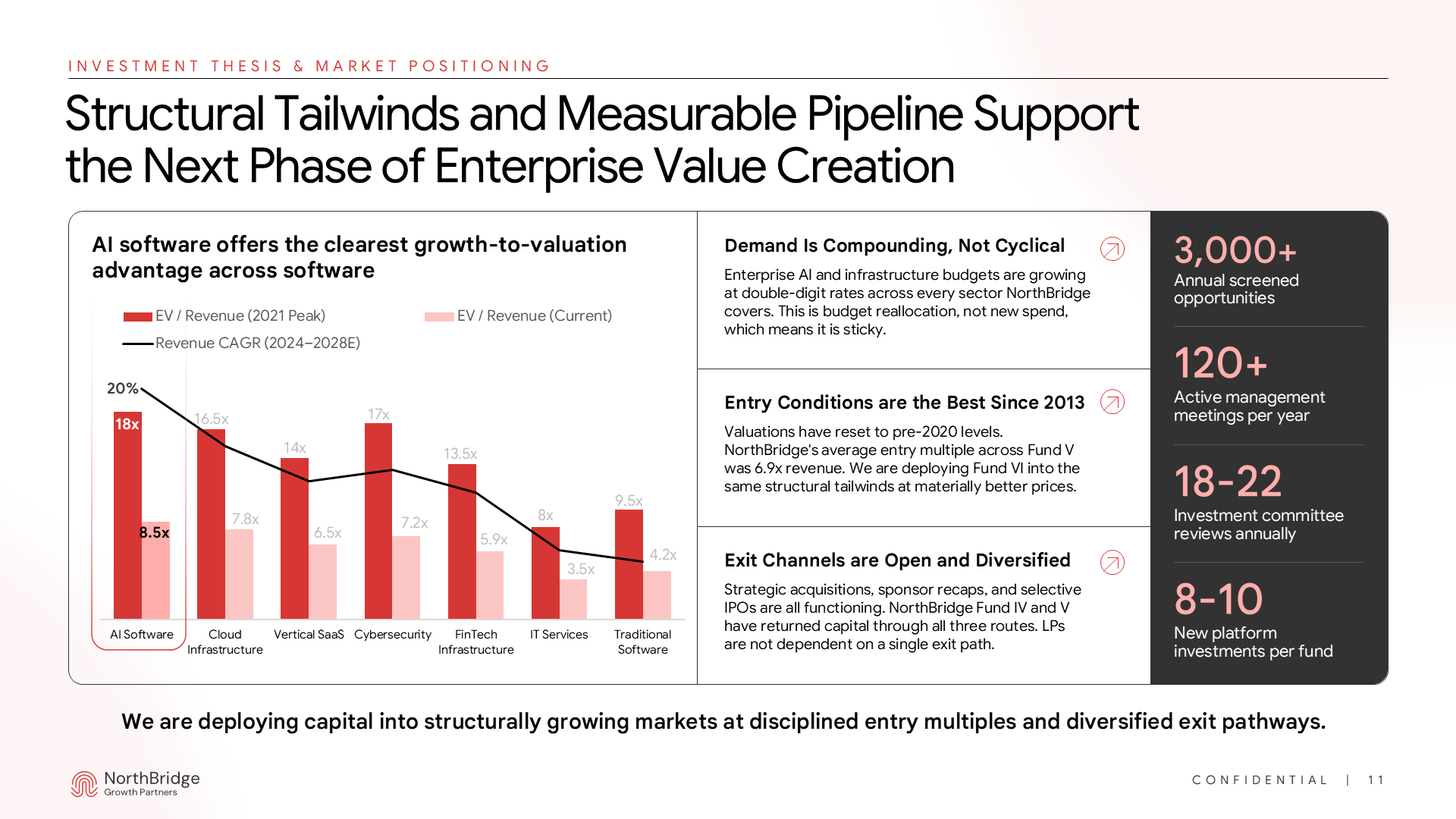

2. Investment Thesis / Why Now

Early Stage

Aspirational “vision of the market,” unique contrarian insight.

Later Stage

The thesis has been tested across multiple portfolios. The slide should show evidence of that, not rearticulate the original conviction.

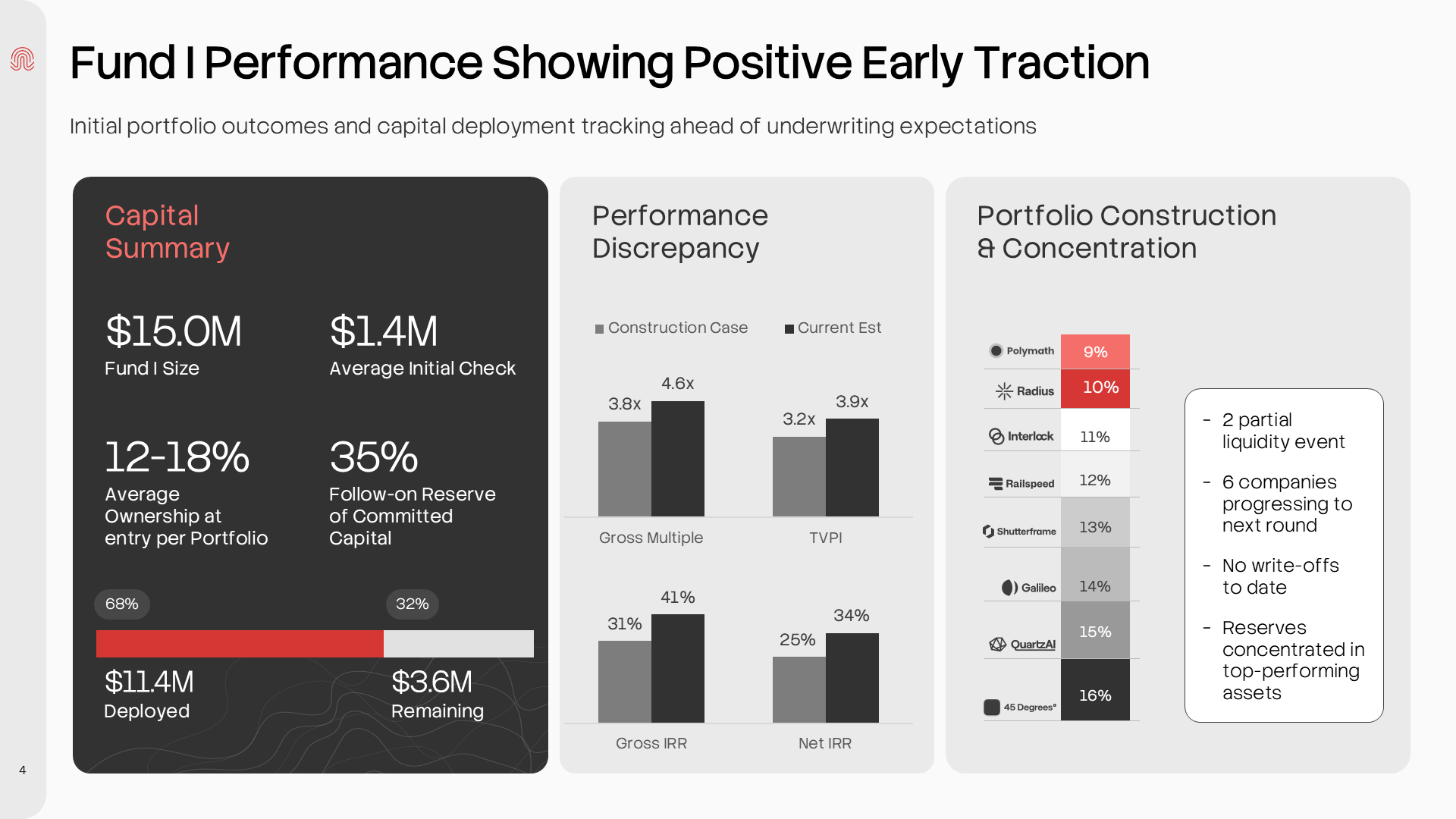

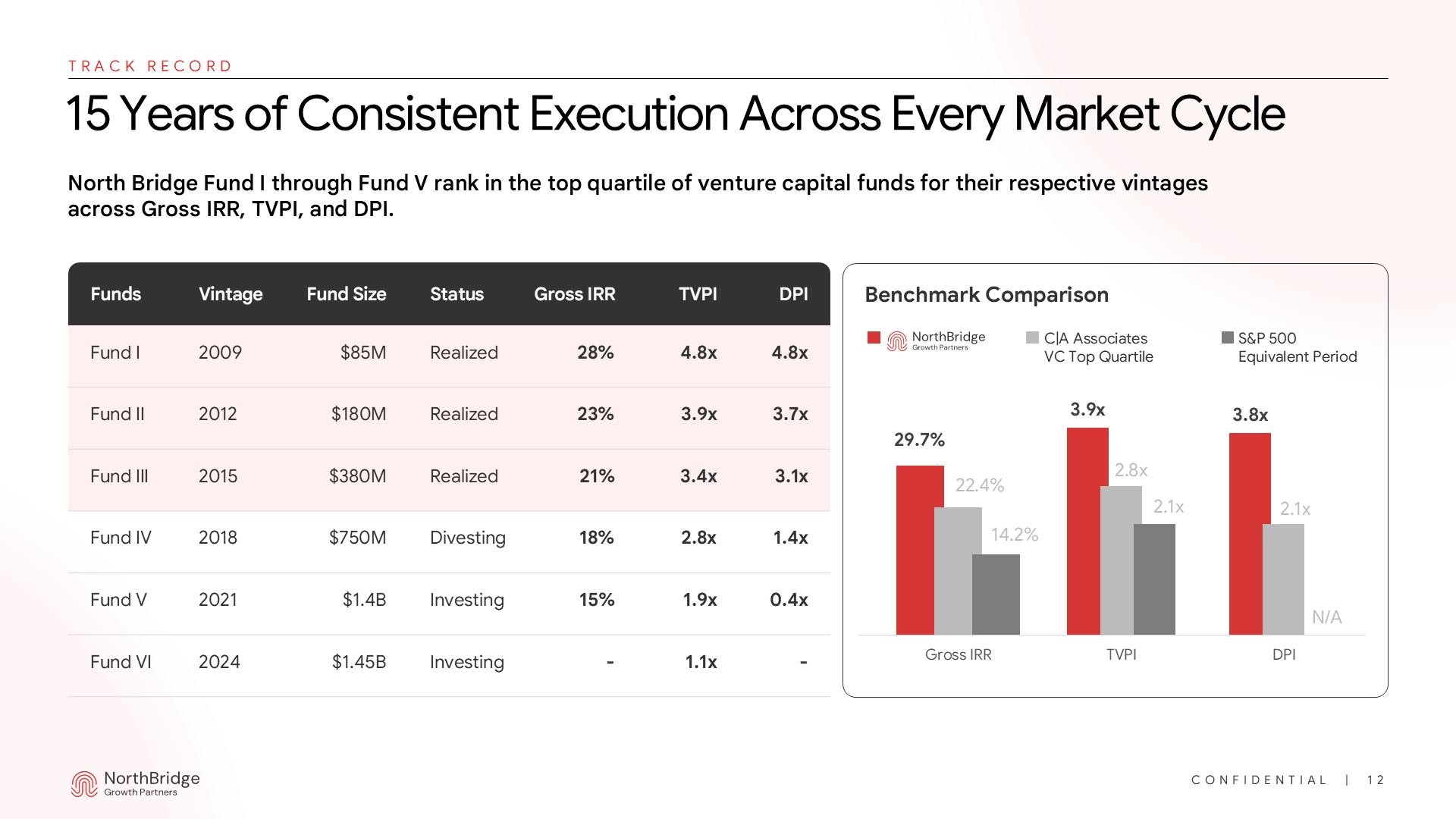

3. Track Record / Performance

Early Stage

The story does the work where the data can't yet. Limited or absent, maybe 1–2 angel deals as case studies.

Later Stage

Every metric that a LP will ask for needs to be here, designed to be read in under 60 seconds.

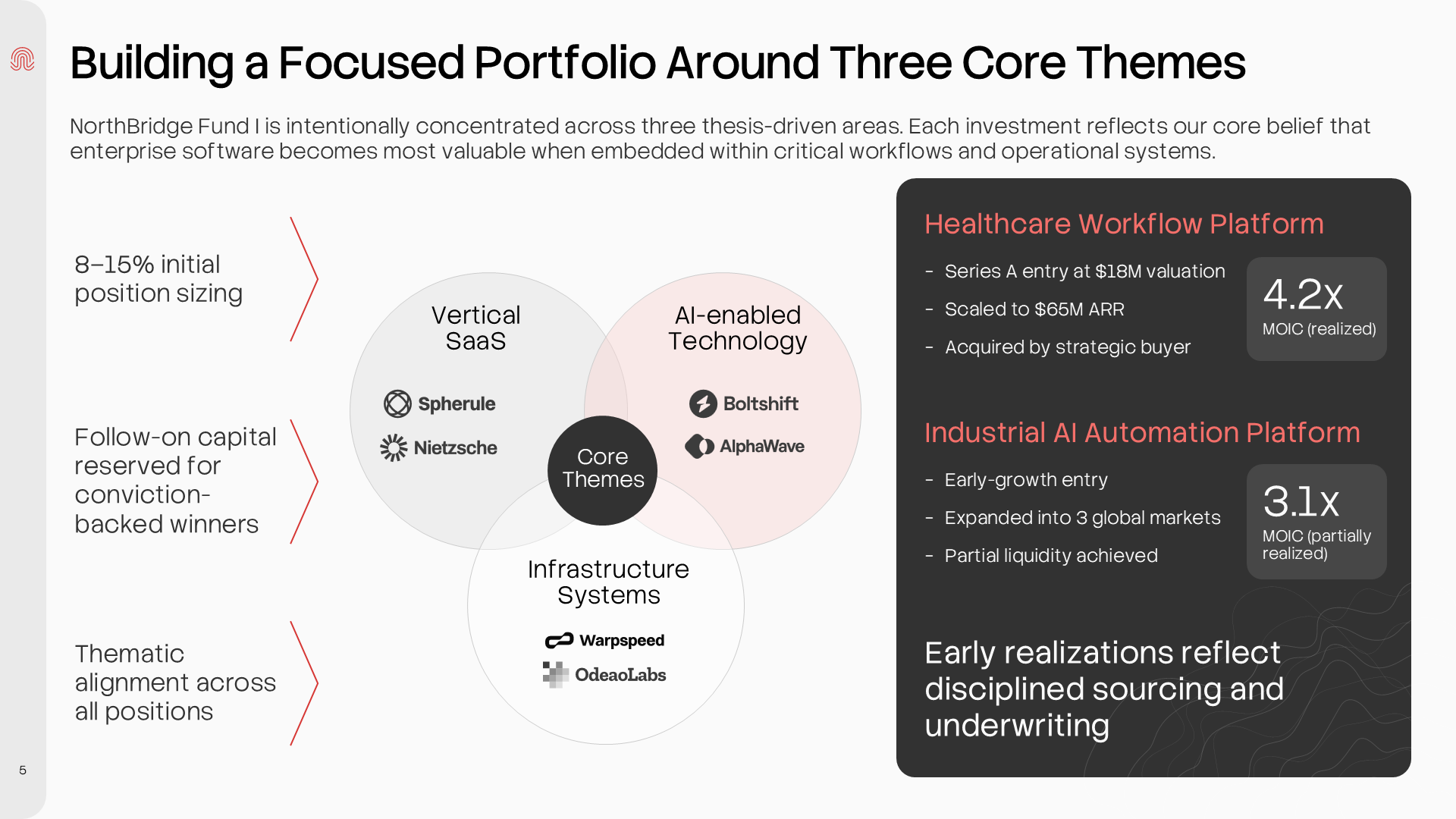

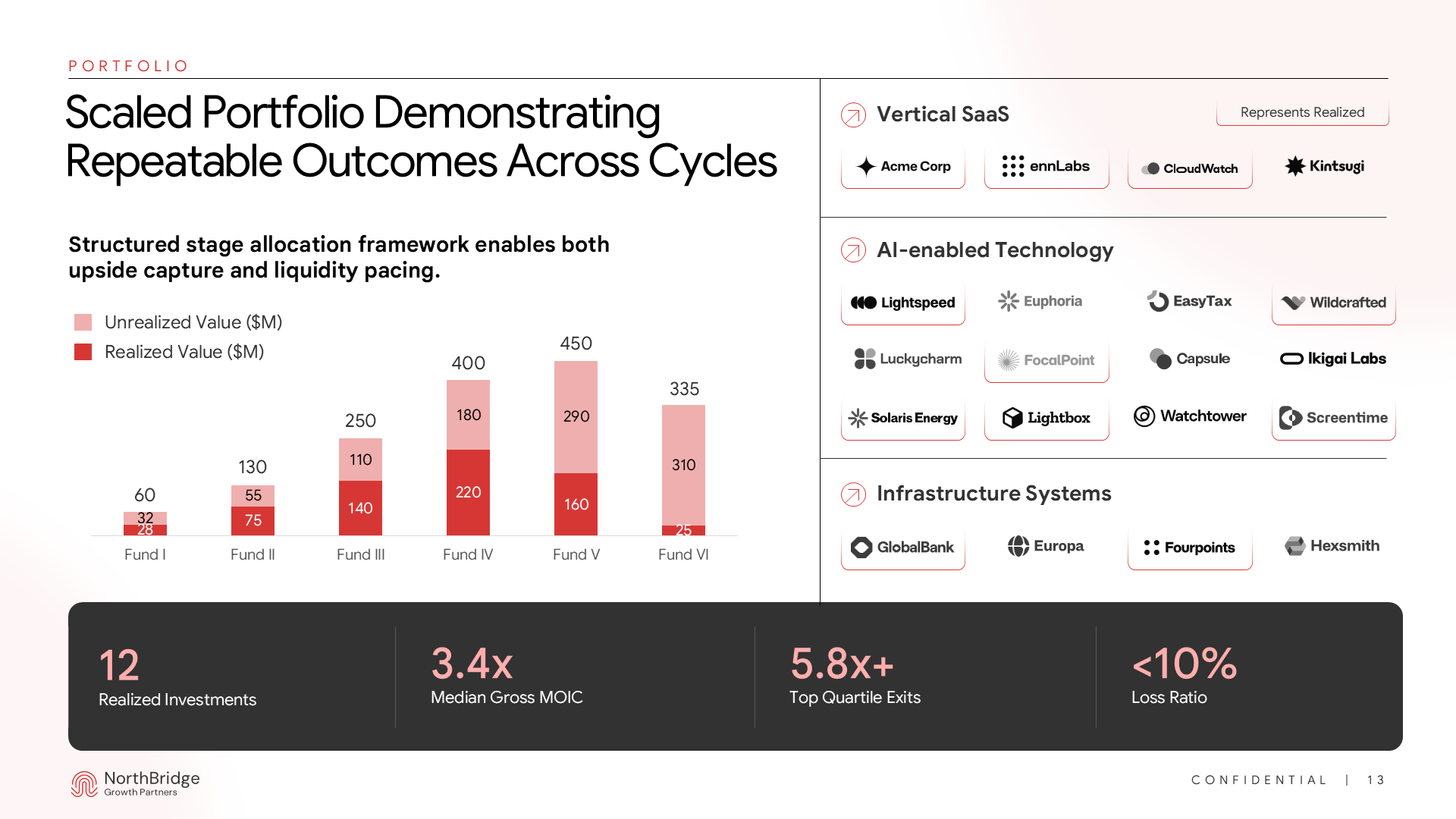

4. Portfolio

Early Stage

The purpose is to demonstrate access, not outcomes. Aspirational pipeline or 2–3 early logos.

Later Stage

The portfolio is proof of the thesis, not an illustration of it. Full portfolio map (dozens of logos grouped by sector).

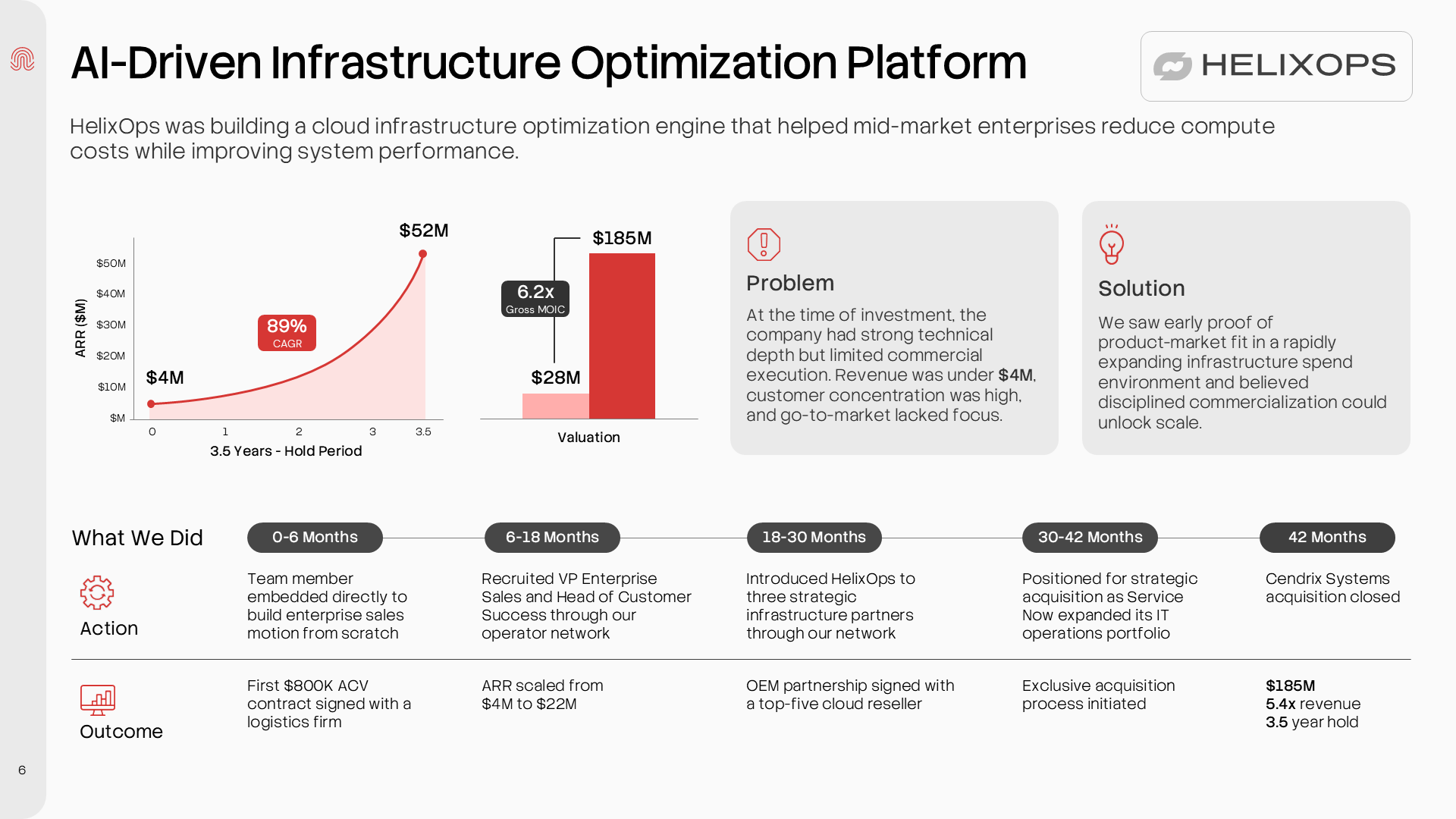

5. Case Studies

Early Stage

Anecdotal stories from prior operating or investing experience.

Later Stage

Deep dives with hard numbers → entry valuation, exit multiple, IRR, value-add.

6. Fund Strategy / Construction

Early Stage

Should be broad and illustrative. "$50M fund, 20 to 25 companies, $1M to $3M initial checks."

Later Stage

Detailed construction logic. Reserve ratios, follow-on strategy, diversification by sector and geography, ownership targets.

7. Value-Add / Differentiation

Early Stage

Commitment-based promises: hands-on support, deep networks, operational expertise.

Later Stage

Institutionalized platform: talent team, market access, ESG programs.

How Design Itself Evolves Across Fund Stages

Most conversations about fund deck evolution focus on content: what slides to include, how to structure the narrative, where to surface the track record. Those decisions matter. But there's a layer underneath them that most firms never address consciously.

It's the design: Typography, color, data visualization, layout density, imagery, iconography. These are not aesthetic preferences. They are credibility signals. And they shift significantly between Fund I and Fund VI.

The underlying principle across all of it: Fund I design is asking LPs to trust you. Fund V design is asking them to verify you.

Bring it Together for Your Next Raise

The gap between where your deck is and where it needs to be is almost always invisible from the inside. The team knows the story. They believe the thesis. The track record feels self-evident. What's easy to miss is that an LP reviewing your materials is not evaluating your firm in isolation. They're evaluating it against every other manager at that stage, with that strategy, at that moment in the market.

According to PitchBook's 2025 LP Sentiment Survey, 68% of institutional LPs cite deck clarity and data presentation quality as a direct factor in their initial interest level, before any management meetings. The deck is the first signal of whether this team understands the level of scrutiny they're operating in.

Design is not the last step. In most fundraising processes, it gets treated as finishing step. The firms that raise cleanly treat it as structural. How information is sequenced, how performance is presented, how risk is surfaced. These are design decisions that shape how the deck is read before a single word lands.

At M'idea Hub, we specialize in fund pitch decks for VC and PE firms at every stage of the fundraising cycle. We have worked with emerging managers establishing credibility for the first time and established platforms making the case for a 9th fund.

If you are heading into a raise and want a second set of eyes on your deck, whether it is your first raise or your fourth, we are happy to take a look. Book a discovery call

Frequently Asked Questions